Captive insurance offers businesses with strong risk management a more cost-effective alternative to traditional insurance, with tax-deferred investment income

Learning Objectives

- Qualification criteria: Learn what is needed to join a group captive.

- Operational structure: Understand how group captives operate.

- Financial benefits: Discover how members can benefit from captives in multiple ways..

Captive insurance insights

- By forming or joining a captive insurance plan, engineering firms can reduce costs, reclaim unused loss funds and benefit from long-term price stability.

- Considering various options allow engineering firms to benefit and possibly save money.

Insurance premiums are on the rise. U.S. commercial insurance prices jumped 7.7% in Q1 of 2024, marking the 26th consecutive quarter of premium hikes.

And engineering firms are feeling the pinch.

Even firms with robust risk management practices and minimal claims are still paying significant annual premiums for commercial general liability (CGL), workers’ compensation (WC) and automobile liability and physical damage (AL/PD) insurance, without many reductions in renewal premiums or dividend payouts.

Have an excellent loss history? Traditional commercial insurers still cannot offer premium levels that match your business’s low risk and often actually rely on these low-risk accounts to subsidize higher-risk insureds.

More engineering firms that feel they are not receiving fair pricing are turning to a different type of policy: Captive insurance. Engineering firms with good loss histories and effective risk management practices can anticipate significant savings upon joining a captive, which often increase over time. On average, a captive member’s initial premiums are approximately 15% to 30% lower than traditional insurance.

What is captive insurance?

A captive is a type of alternative risk transfer where the insurance company is owned by the businesses it insures. This ownership structure gives business owners control over their insurance programs, allowing for superior risk management at lower costs.

There are two main types of captives: single-parent captives and group captives.

- Single-parent captives are owned by one business, which manages the captive independently. This is typically suited for large, complex organizations.

- Group captives are jointly owned and controlled by multiple businesses, often mid-sized to large companies, insuring specific risks at reduced rates. Group captives can be either homogeneous (similar types of businesses from the same industry) or heterogeneous (various types of businesses from different industries).

Group captive insurance differs significantly from traditional insurance in structure. Premiums in group captives are primarily based on recent individual loss data rather than exposure formulas or mandated rates, as is common with traditional insurance.

These premiums are used to create loss funds that cover claims for both the individual company and all captive members in a shared risk pool at different loss levels. Group captives typically provide coverage for common lines of insurance: CGL, WC and AL/PD.

Group captive members share a crucial characteristic: historically low losses. To qualify for a group captive, firms must demonstrate the following attributes:

-

Effective risk management. Businesses must engage in proactive risk management, such as using telematics for fleet safety and implementing robust controls around driver selection and job site safety.

-

Good loss ratios. Candidates should have a loss ratio below the industry average of 50%, unless there is an outlier claim that inflates their score. In such cases, proper justification must be provided. The loss ratio is assessed for each line of coverage over the past five years, using exposures relevant to each line of coverage to benchmark an organization’s losses against similar businesses.

-

Meet minimum premium requirements. Group captives typically require a minimum combined premium, which often starts at $250,000.

Group captive insurance offers numerous benefits

Engineering firms might join a group captive because they are frustrated with overspending on premiums in the conventional marketplace. They seek an alternative that offers greater long-term control over their premium and risk management costs.

As the reduction in premiums becomes more aggressive, the gap between traditional insurance costs and captive insurance widens significantly. After three to four years of participation in a captive, policy periods typically mature, allowing insureds to reclaim unused loss funds as dividends, leading to even greater savings.

For well-performing firms, these benefits compound over time, offering long-term price stability, reduced renewal rates. It also incentivizes firms to improve loss prevention and risk management practices to further lower claims costs. In addition, premiums and other member contributions are invested in a multibillion-dollar investment fund, providing captive members with the potential for significant tax-deferred investment income returns.

How group captives operate

This nontraditional risk transfer model has annual terms like traditional insurance, but that’s where the similarities end. Group captives typically operate using a committee structure (including executive, finance, risk control and underwriting committees) where each member company has one vote regardless of premium size and decisions are made by a simple majority. No external parties — such as the fronting carrier, the reinsurance carrier or any captive resources — have voting power.

Each member firm appoints a director to participate in meetings and vote on behalf of their organization. Most captives are domiciled in Bermuda or the Cayman Islands due to favorable corporate tax implications, stability under British law and straightforward regulation, creating a business-friendly environment. Board meetings usually occur twice a year for members to decide on various aspects of running the group captive. These meetings also provide opportunities for peer networking and renewal presentations with clients.

Each year, member premiums are pooled together, with approximately 65% allocated to loss funds for claims and about 35% used to cover operating costs, including claims administration, fronting and reinsurance, risk control, actuarial services, accounting, board meetings and group captive management.

Each member has a risk control fund, funded by 1% of their annual premium. Firms can use their risk control fund to improve risk management outcomes in various ways, including but not limited to training and policymaking for general and site safety, telematics implementation costs, industrial hygiene and ergonomic assessment.

An appointed risk control consultant conducts an assessment for each firm every three years and provides suggestions on how to best use their funds to enhance their performance.

Group captives: An enticing alternative

Group captive insurance offers an innovative risk transfer solution for midsize to large businesses with historically low loss ratios and excellent risk management practices. With premiums based primarily on each member’s actual losses, group captives reward disciplined risk management and incentivize individual performance. By creating your own insurance companies, engineering firms can gain greater control over their insurance programs, reduce costs and earn tax-deferred investment income.

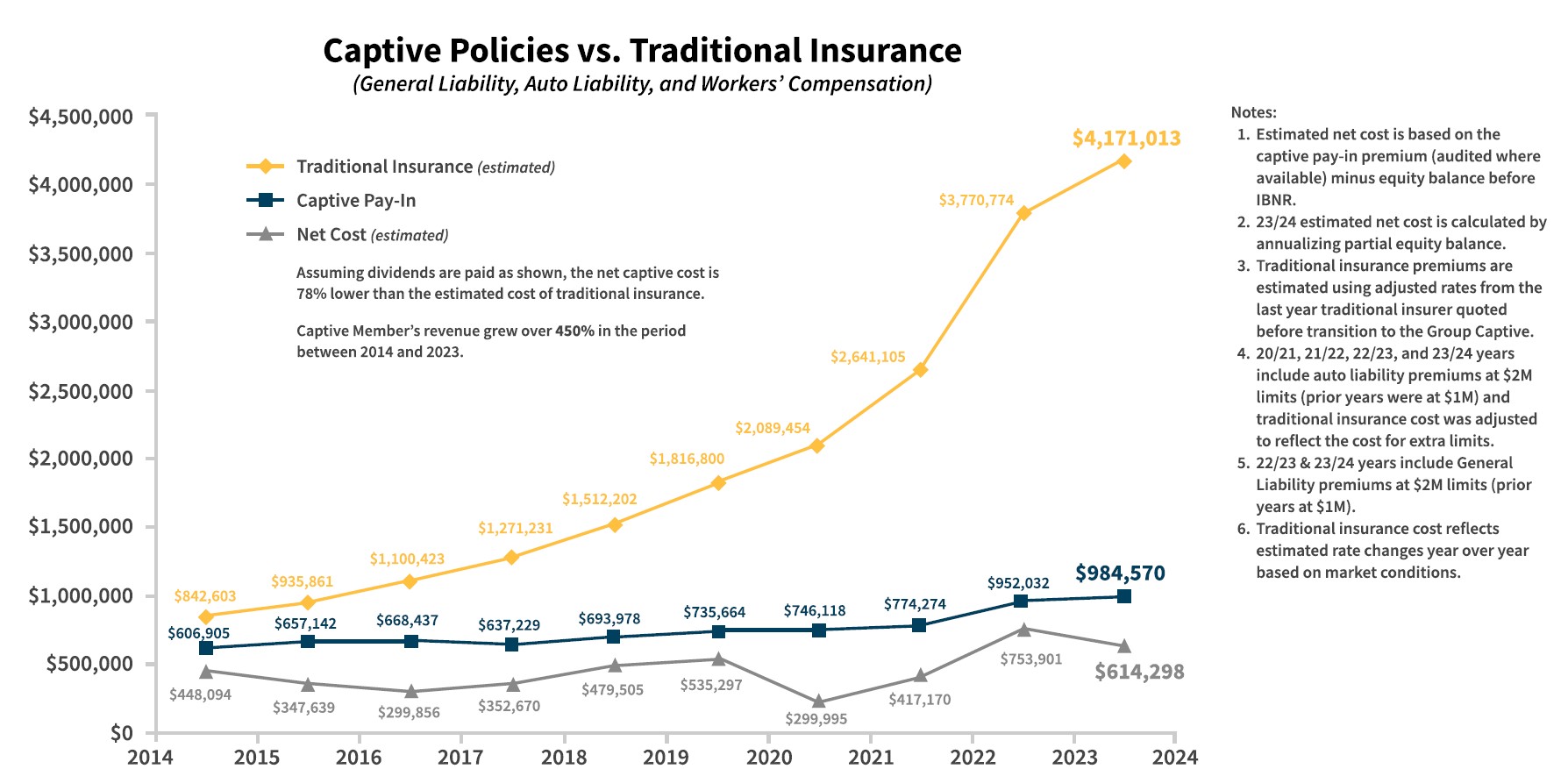

For example, one architecture, engineering and construction firm achieved an incredible 78% reduction in costs compared to traditional insurance, resulting in nearly $16 million in cumulative savings over a 10-year period through group captive participation.

As illustrated in Figure 2, the firm’s captive pay-in (blue line) was significantly lower than traditional insurance costs (yellow line) throughout this period. Additionally, the business’s revenue increased by 450% over nine years, substantially increasing the savings as a result. The firm’s net costs (grey line) were further reduced by captive dividends and equity payouts.