Mechanical, electrical, plumbing (MEP), and fire protection engineering firm leaders continue their merger and acquisition pace in the United States, while overseas activity weakened in 2013.

Last year, we boldly declared that mergers and acquisitions (M&A) were back among the MEP Giants, as a sense of optimism led to a flurry of deal-making in 2012. Throughout 2013, Consulting-Specifying Engineer’s MEP Giants remained in the M&A game, with 16 of the giants acquiring a firm in 2013—the same total as the prior year. The positive economic vibes that prevailed in 2012 have rolled on through 2013 and have continued so far this year. The 2014 MEP Giants continue to make calculated moves to advance their strategic positions through M&A.

Domestic deals remain steady

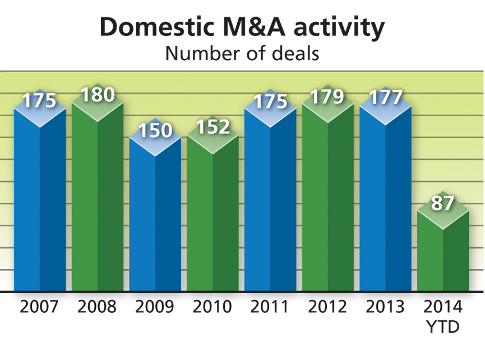

Steady M&A activity among the MEP Giants aligned with strong and steady U.S. domestic M&A activity for architecture, engineering, and construction (AEC) firms in all sectors. The 177 domestic M&A deals reported in 2013 (deals involving a U.S.-based seller) mirrored the activity from the prior year (see Figure 1). These levels have remained generally in line with the 180 deals reported at the heights of 2008 and prior to the Great Recession.

Industry firms appear to remain cautiously optimistic, with deal activity in 2014 on pace to rise to similar levels by year-end. Project opportunities continue to flow, both in the public and private sectors, but the approach among project owners appears to be more measured than the breakneck pace of building that led up to the bubble bursting in 2008. As of July 2014, the Dow is at an all-time record high, which has led many to pause and reflect on which way the economic wind is blowing. The overall economy appears to continue to move forward, albeit one slow, deliberate step at a time.

The MEP Giants continued to take advantage of the positive economic climate by making strategic deals in 2013 that advanced their market positions, expanded their service offerings, and opened them up to new geographies. Two deals MEP Giants made in the past year included:

-

MEP Giant No. 10, Arup (New York City and London) integrated Artec Consultants (New York City), an acoustics, audio-visual, and theater consulting firm, into its New York Arts and Culture practice.

-

Henderson Engineers (Kansas City, Mo.), this year’s No. 13 MEP Giant, acquired health care-focused MEP and fire protection engineering firm Corporate Energy Consultants (Shawnee Mission, Kansas).

A tale of two markets: Overseas deals weaken

International M&A activity (deals involving a non-U.S. based seller) were another story entirely in 2013. Overseas deals declined 18% in 2013 when compared to 2012 (see Figure 2). This slide began in 2012 and worsened in 2013, with economic uncertainty dragging down deal-making in many parts of the world. The Eurozone economy continues to grow more slowly than expected and has led the European Central Bank to step in, in an attempt to give the European Union a shot in the arm.

The BRIC countries (Brazil, Russia, India, and China), once touted as the next great global economic engines, have lost considerable steam, with many investors looking to a strengthening and more stable West for development opportunities. Brazil’s status as a global darling among foreign investors has begun to lose momentum. Russia’s situation has become even more uncertain, with potential economic sanctions looming in light of the intervention in Ukraine. Mass corruption and a looming loan crisis have bogged down India’s continued growth. Massive overbuilding of infrastructure and factories in China has created a bubble that many analysts believe will be the next to pop. This has led buyers to look for more stable environments with a lower risk profile for deals.

The United Kingdom, Australia, New Zealand, and South Africa are a few of the bright spots globally, combining for 46% of the international deals we tracked last year. Perhaps the biggest splash in the AEC world in 2013 was MEP Giant No. 1, Jacobs’ (Pasadena, Calif.) merger agreement with 6,500-person consulting, engineering, and project delivery firm Sinclair Knight Merz (SKM) (Melbourne, Australia) for approximately $1.2 billion. The deal was among the largest reported in 2013.

Beyond SKM, Jacobs has recently made several deals domestically in the telecom sector. Last year, Jacobs acquired specialist wireless telecommunications infrastructure design and construction firm Compass Technology Services (Atlanta) and has added 750-person Federal Network Systems (FNS) (Ashburn, Va.), a subsidiary of Verizon Communications, and FHMC Corp. (Chicago), a provider of turnkey wireless communications services. These were among nearly 10 total acquisitions for Jacobs in 2013 and thus far in 2014.

The shift back to the U.S. as a growth market played out in 2013 as 17 international buyers bought a U.S. firm versus just 12 U.S. firms buying overseas. This reversed the trend set in 2011 and 2012, as U.S. firms sought to expand internationally at the same or greater pace than overseas firms did in the U.S. So far in 2014, it appears the U.S. is outweighing overseas markets as a desirable target for international M&A expansion (see Figure 3).

Interstate deal traffic climbs in 2013

Interstate deal activity (firms from two different states merging) jumped significantly in 2013 (see Figure 4), rising close to a level not seen since 2008. This is a strong indicator that firms were officially out of the trenches and looking to expand to new markets and clients beyond their existing footholds. During the recession, interstate activity dipped, as firms made defensive moves to maintain revenue and market share. In 2013, firms crossed state lines to capitalize on new growth opportunities, going back on the offensive. Interstate activity is down slightly so far in 2014, and it remains to be seen how that plays out through the remainder of the year, as buyers carefully consider their next moves.

MEP Giants continue consolidation trend

Once again, 16 of the 2014 MEP Giants reported making acquisitions this year. Notable among them were several deals that further consolidated MEP services among the Giants. MEP Giant No. 40, Gannett Fleming (Camp Hill, Pa.) acquired multidisciplined facilities engineering, commissioning, and energy efficiency firm Griffin Engineering and Technical Services (Morrisville, N.C.), which became part of Gannett Fleming’s national mechanical and electrical practices. MEP Giant No. 68, P2S Engineering (Long Beach, Calif.) acquired health care-focused MEP and fire protection engineering firm Donn C. Gilmore & Assoc. (Anaheim, Calif.).

MEP Giant No. 7, Stantec (Edmonton, Alberta) was among 2013’s most active dealmakers, notching 7 deals over the course of the year. Notable among them was Stantec’s acquisition of the assets of IBE (Sherman Oaks, Calif.), a 50-person building engineering firm that specializes in high-performance sustainable design of MEP systems. In early 2013, MEP Giant No. 26 EYP (Albany, N.Y.) merged its energy and sustainability services division, EYP Energy, with The Weidt Group (Minnetonka, Minn.), a building energy and software consultancy. Consolidation has continued in 2014 as KCI Technologies (Sparks, Md.), this year’s No. 66 MEP Giant, acquired Redding Linden Burr (RLB) (Houston), an engineering company specializing in MEP and energy services.

Consulting-Specifying Engineer’s MEP Giants remained on the offensive in 2013, adding services to complement their existing offerings and expanding into new territories. High-performance buildings, which aim to optimize energy and water use, have become expected among project owners, and the MEP Giants continue to focus on high-performance HVAC, electrical, and plumbing design capabilities to meet owners’ needs.

What’s ahead for AEC M&A?

Does M&A activity continue at the current pace? Does it cool off as the U.S. economy has perhaps plateaued? It appears AEC industry firms are taking the cautious approach and making deliberate acquisitions that are strong contributors to their strategic objectives. We anticipate that activity will remain steady through the remainder of the year, with deal activity concentrated in the U.S. and select overseas markets.

Depending on the evolving conditions in the Eurozone and BRIC countries, overseas M&A may pick up if some level of stability is reached in those economies. We anticipate more firm owners will want to go out on top after many firms have had an opportunity to build a track record of several years of solid performance since the recession. Many owners will likely seek to exit at what they feel may be a high watermark for their business. This will likely create more opportunities for buyers to seek and close deals selectively as owners look to transition ownership and leadership. This, coupled with continued globalization and the accelerated rise of alternative delivery methods, is expected to create an environment where AEC industry consolidation will continue steadily for the foreseeable future.

Neil Churman is a principal consultant at Morrissey Goodale LLC, a management consulting and research firm that exclusively serves the AEC industry. Based in the firm’s Houston office, Churman is a certified M&A advisor and works with AEC firms to deliver consulting and advisory solutions.