Performing a series of cost analyses when designing HVAC systems is an economically justifiable method to selecting the appropriate design solution.

In too many of today’s new and retrofit projects, short-term thinking and lack of rigorous financial assessments result in the irrevocable loss of opportunity for sound financial returns. Although not all high-performance strategies will have a financial basis, many that do are often overlooked. Returns that range from 10% (7-year payback) to 30% (2-year payback) are available at risk levels far below investments offering comparable returns (e.g., the stock market’s 9% historical return and venture capital’s historical 30% return).

The challenge is that such positive returns often come in the form of new ideas, technologies, or processes that cost more upfront, hence the need for a “return.” Clients and investors are often concerned by such innovative ideas because of their increased upfront costs. As a result, designers are called on to inform clients of design options from a performance and financial perspective.

Lifecycle cost analysis (LCCA) provides a method of quantifying the performance over the design lifetime. It also provides an insight into the secondary benefits of a proposed design, for example, reduced maintenance, complementary systems, improved environmental quality, and so on. It is a powerful and flexible tool that takes time and expertise to extract value. For all its positive potential, in the wrong hands, it can make a good investment look bad. Or perhaps worse, make a bad investment look good.

Typically, when used in design, LCCA is performed early in the process to assist in determining the appropriate design solution. At this stage of the process, the information available is generally not detailed or fully developed. The common adage thus applies; the output of an analysis is only as good as the assumptions that are used to develop it. Therefore, the real power of LCCA is in the ability to compare different solutions for a set of given assumptions.

The fruit of this comparative analysis is typically a set of discounted cash flows over a given period time. Analysis can range from a simple study with very few variables to a complex analysis with hundreds of variables in a parametric study. Even in the most detailed of studies some intangibles cannot be adequately evaluated. So often answers are given as a range, and thought must go into the decisions as well as the analysis.

Technologies that would have previously required an LCCA but are now commonplace include variable frequency motor drives, spectrally selective double glazing, economizer cycles, florescent light bulbs, and further afield Hybrid Drive technology on cars. Technology that might fall into that category as prices drop includes solar technologies, LED lighting, radiant heating and cooling, and carbon fiber structures.

As with almost everything, the more complex the problem, the greater effort required to keep the conclusions simple. The best outputs are the ones that are most transparent. KISS: Keep it short and simple.

LCCA basics

We’ve avoided writing too much detail on LCCA since there are such excellent books on the topic. However, we did feel that it would be beneficial to summarize some of the key terms and concepts as a refresher for those already familiar and as an introduction for those just getting their feet wet.

Lifecycle analysis (LCA): The LCA process considers all costs and benefits (economic, social, and environmental) over the course of an investment life. It is generally accepted as different from a lifecycle assessment, which is a technique to assess environmental impacts associated with all the stages of a product’s life from cradle to grave. LCA includes LCCA.

LCCA: LCCA focuses on economic costs over the course of the investment life and includes a variety of methods for determining if an alternative is economically justified. The methods of LCCA include:

- Lifecycle costing (LCC): LCC is a present value sum of all the costs incurred over the life of an investment. Alternatives must be mutually exclusive (e.g., solar hot water system versus an on-demand hot water heater system), and a first-cost budget may constrain selection of the optimal investment.

- Net savings (NS): NS is a current value expressing the net lifecycle benefit after costs are subtracted. Alternatives must be mutually exclusive, and a first-cost budget may constrain selection of the optimal investment. NS will return the same optimum selection as LCC, but a defined baseline is needed on which to base the net calculation.

- Savings to investment ratio (SIR): SIR is a ratio expressing the multiplier by which savings exceed the cost of investment (i.e., an SIR of 1.1 indicates that savings exceeded the cost of investment by 10%). SIR may be used to rank non-mutually-exclusive alternatives (e.g., high-performance glazing, improved insulation, efficient air distribution, etc.)

- Return on investment (IRR or AIRR): A measure of annual percentage yield from an investment. ROI and SIR are the optimal methods used to rank non-mutually-exclusive projects.

- Discounted payback (DPB): The time required for an investment to be fully recovered. Discounted payback incorporates the time value of money (i.e., future money is worth less than present money, and must therefore be discounted to present value). DPB is best used for screening multiple alternatives. It should not be used for final selection.

- Simple payback (SPB): The time required for an investment to be fully recovered. Simple payback does not incorporate the time value of money and is often inaccurate. Although used for back-of-the-napkin discussions and rough comparisons, it should not be used for final selection.

LCCA nuances

There are many methods for helping a decision maker navigate the myriad of options in a project. LCCA is the only method that can assess the economic return of a given strategy and begin to form the basis for investment grade analysis. It is typically used on a small set of options that have reasonably detailed cost and savings estimates. Due to the effort typically involved, it is generally reserved for high cost/value decisions where the cost of analysis is equal to or less than the first year potential savings. Since the quality of the analysis is shaped by the degree of detailed information available, judgment is needed to determine how early or late in a design process the analysis should occur. Too early, and the quality of information is inadequate. Too late, and the critical path of decision making is impacted. More than any other method, LCCA can be misused and misinterpreted.

Knowing when to apply LCCA

As with any tool, knowing when to apply LCCA is critical to success. The potential savings should be great enough to justify the analysis costs, which can vary significantly across projects. There should also be adequate information and expertise to assure the output is valid.

The decision as to what type of LCCA method is most appropriate is also necessary. As discussed elsewhere in this article, the various methods, such as LCC, NS, AIRR, SIR, DPB, and SPB, each have their own strengths, weaknesses, and limitations. Often, clients have preferred methods.

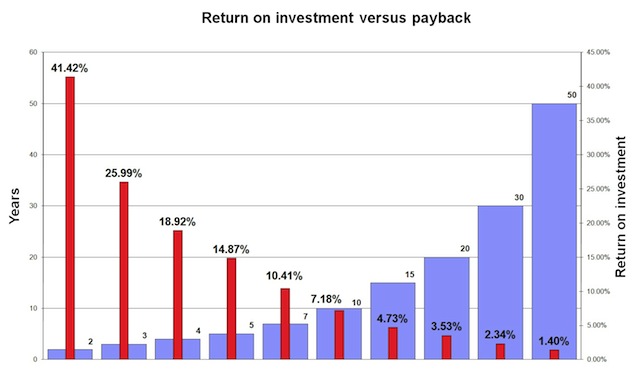

The dangers of payback

Too many buildings are constructed with only a cursory review of the payback of an investment. Although many of these decisions may be good ones—a fast payback is often a good investment—a significant percentage will not result in an optimized return for the owner due to inaccuracies in the analysis. More worrisome still is that many investments that have a longer payback are often discarded, despite being financially attractive.

The reason for this failing is that payback calculations look only for the date at which break-even occurs, a full recovery of the investment. They do not consider costs and benefits that may occur preceding or following this break-even point, nor do they consider the budgetary implications. As the graph demonstrates, the best investment may not be the one with the fastest payback.

Protecting your return

It is critical in any LCCA that some discussion of sensitivity takes place. The discussion becomes all the more important for those decisions that show a potential for significant costs or that are perceived to be of elevated risk.

Sensitivity analysis can take a number of forms:

- Testing of the impact when input variables are modified

- Testing optimistic and pessimistic scenarios

- Testing maximum and minimum values for variables in order to establish a likely range of potential outcomes.

Offsetting

Considering the building as a whole, a collection of systems dependent on and interacting with one another, gives rise to the strategy of offsetting costs. This is especially true of systems that are eliminated from the building due to the increased efficiency of other systems. Through system elimination, the first cost can actually be reduced. Examples include tile roofing displaced by a photovoltaic system, reduced floor-to-floor height due to a radiant conditioning system, or reduced ductwork and MEP system capacity due to natural ventilation.

A single budget

The importance of connecting the capital pool assigned to construction with that assigned to ongoing maintenance and operation (at least in concept if not in accounting practice) is a critical first step to assuring potential investments are not missed. Without it, short-term first-cost priorities will outweigh the value of long-term savings.

Minimum acceptable return and risk

Investors vary greatly in their financial expectations, reflected in their minimum acceptable rate of return (MARR). The catch is that all too often the MARR that people quote (also often called the discount rate) is not the one they should quote, because they forget that a MARR is qualified by the risk or uncertainty of the anticipated future cash flows. For a risky investment, the MARR should be high. For a low-risk investment, the MARR should be low.

Unfortunately, the minimum return used to determine project feasibility is often set inappropriately high, leading to the undesirable elimination of otherwise attractive investments. Fortunately, many investments in HVAC systems are actually low risk. Energy efficiency is correspondingly certain when compared to investing in new equipment, products, or businesses.

The real MARR for energy conservation measures (ECMs) should typically be in the 3% to 7% range unless third-party financing costs push it higher.

Other possible topics

The above are only a few of the nuances of effective LCCA. At the conclusion of this article, additional reading is recommended, which includes discussion of a variety of topics, including:

- Comparing designs that have different lifetimes

- The impact of tax liability and third-party financing on investments

- Constant versus current dollars and nominal versus real interest and escalation rates.

Conclusion

As demonstrated by the examples above, LCCA can provide a valuable tool in assessing the appropriate technologies and techniques for maximizing the value of a project. It can help ensure an investment is secured in the options that are most likely to result in the largest returns for the extra investment. Accuracy and diligence in the selection of software and inputting the variables to be considered can ensure that a transparent auditable calculation is produced.

However, even the most rigorous results are not infallible predictions of future performance. Results have inherent limits of precision that should prompt questioning. The end goal is for information that is approximately correct rather than precisely wrong.

Particular attention should be paid to single answer results or results that contradict the instincts or previous work on the subject matter. While errors are possible, changes in technology, pricing, and subsidies may have made alternates that were even recently unpalatable, the best investment for your project.

Who knows, you might be reading this article in an LED-lit, radiant cooled, solar powered building, wondering why all buildings haven’t always had these features.

Roberts is an associate principal and energy and resources business leader in Arup’s San Francisco office. His experience ranges from climate-responsive building engineering and consulting to community energy systems, net-zero energy, and climate-positive design. Rhodes is a senior engineer in Arup’s San Francisco office, specializing in high-performance mechanical system design and energy monitoring. Hespe is a senior energy and sustainability designer in Arup’s San Francisco office, specializing in passive and ecological building design.