Commissioning professionals (CxPs) can be defined as technical analysts, bloodhounds, and diagnosticians working to connect ideas and project teams to future buildings and systems. The Building Commissioning Association (BCA) surveyed commissioning professionals who are “giants” in their field due to their advocacy in educational and industry support on behalf their profession.

Learning Objectives:

- Introduce the top commissioning professionals, including the 2015 Commissioning Giants.

- Explain who hires these firms and why, how much their services cost, and what’s changing in the markets they serve.

Often facilitating behind the scenes, the commissioning professionals’ (CxPs) role is to make sure that owners, designers, builders, and tenants get what they planned for by the time a building is turned over for occupancy.

In 30-some years, building commissioning has become a recognized practice in the building community. Now that the overall economy is recovering, commercial and institutional construction starts are wavering slightly but generally trending upward.

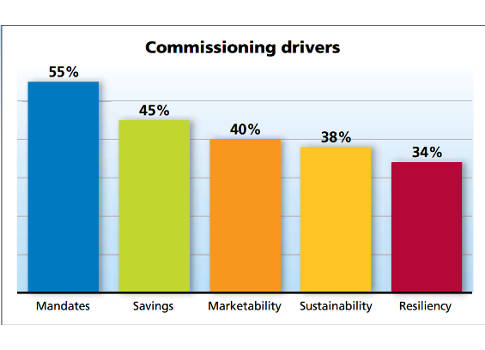

Beyond market expansion, drivers for commissioning are striking owners and the building industry from various directions: increasing demand for energy and financial savings; mandates such as codes, standards, and benchmarking regulation; sustainability; facility marketability for sales and leases; and, due to recent natural disasters, resiliency. In this survey, commissioning firms ranked their opinions of the most important drivers for owners (see Figure 1).

What does this mean? Savings—energy and financial—started out as the only drivers for commissioning back in the day. The increasingly complex issues within the built environment have caused federal, state, and local governments to require commissioning as a way to support both energy savings and "sustainability." New codes and standards, and recent requirements for energy benchmarking, are driving a regulatory atmosphere in the building industry. This now requires a process that delivers owner’s project requirements, project team integration, jurisdictional compliance, and technical capabilities. In today’s building scenario, these can only be provided by a professional who has the skills and knowledge to test functionality, communicate issues, and advocate for building performance across the full scope of a project.

Another driver—existing-building commissioning (EBCx)—started catching up with new-construction commissioning (NCCx) during the recession. Without the resources to build new facilities, owners turned to renovation and equipment renewal inside their existing building shell. EBCx now represents about half of the commissioning projects across the U.S. However, EBCx requires a different set of tools and knowledge to integrate old systems with new. Most commissioning firms focus on one or the other.

Whole-building commissioning (WBCx)—the process of ensuring comprehensive, integrated performance of all building systems and components before turnover—is recommended by organizations such as the National Institute of Building Sciences. WBCx is slowly maturing, but as opposed to discrete systems commissioning, is not at all universally practiced.

Commissioning authorities or agents (CxAs) themselves are experiencing challenges to their portfolio of services as a result of innovative technologies and changing regulations. Questions about the future abound: Is it cost-effective to retain specialty staff in-house? Do we need to be certified and, if so, by whom? What codes are affecting the services of commissioning providers? Is our profession becoming commoditized? If so, how do our qualifications stand up to a low-bid selection process?

Finally, the big challenge for the commissioning profession is to attract and mentor candidates who will build a new generation of CxPs. This profession doesn’t require licensure, yet it requires skills and abilities that are not readily available from new graduates. As one survey respondent put it, "It’s like trying to find a unicorn."

Survey findings: sectors, systems, and services

Sectors—Most companies surveyed are involved in more than one market sector (see Figure 2). The private sector predominates at 51%, followed by public (government) buildings at 29%. The remaining 20% represents higher education (18%) and industrial markets. All CxPs except those committed to a single building type, such as data centers, commission office buildings. On the other hand, retail (grocery stores, shopping malls, and restaurants) represents less than half of respondents’ commissioning business; specialized HVAC and refrigeration requirements and the duplicative chain retail environment may cause owners to hire specialized, long-term providers/advisors for their portfolio of facilities.

Systems and services—The study shows that 57% of responding firms provide commissioning services on "discrete systems," while 43% say they are practicing "whole-building commissioning." On an individual basis, most companies split their services approximately 80/20 in one direction or the other, with a few reporting they perform only WBCx or only discrete systems-only work. WBCx is not well-defined as yet. Although the term implies that commissioning teams will comprehensively work with design and construction teams, understand the integration and perform testing for all building systems prior- and post-occupancy, this may not be the rule even for those who report that they conduct WBCx.

Twenty-five percent of respondents conduct all commissioning services in-house. Generally, they are large, multidisciplinary firms with more than one office location nationwide. Most frequently, building enclosure (BECx) is outsourced due to the architectural and engineering decisions related to the building shell and integration with design and protective features from belowgrade to the top of the building. BECx represents 65% of services hired out in commissioning, followed by fire and life safety, plumbing and water, and elevator systems.

Follow the money

Respondents were asked to estimate their firm’s overall volume of annual building-commissioning contracts, excluding design and construction costs, equipment retrofits, and replacements. All but five companies reported their project volume, which ranged from three to 450 annually. Paired with additional information from each firm, such as estimated number of projects per year, annual fees per year, and square footage commissioned per year, the reported projects (with the exception of several outliers) range from $25,000 to $300,000 for commissioning fees. The majority of projects were estimated at less than $1/sq ft cost to commission.

Some building types require significantly more commissioning on a square-foot basis than others due to complexity, purpose, occupancy requirements, and location, among other characteristics (see Figure 3). One firm reported, on average, that they perform eight commissioning projects for a total of $115 million, covering 750,000 sq ft of building space. Averaged out, that comes to $14.4 million/project at a cost of more than $19/sq ft. These are likely highly specialized facilities. In a more typical scenario, another firm reported seven projects averaging 40,000 sq ft at a cost of $50,000 to commission —$1.25/sq ft. It’s all about context.

Today, commissioning is increasingly integrated with project design, construction, and operation, but the survey shows that the construction phase remains by far the predominant commissioning service (see Figure 4). As building systems, including enclosure, become integrated through increasingly complex controls systems, there is pressure for CxPs to become engaged prior to design. By working with the owner and design team, the A/E basis of design and owner’s project requirements can be correlated to provide a clearer roadmap for achieving the design and operation envisioned by the owner. Despite the obvious benefits, many of which could cut owners’ costs during and after construction, there is a cost associated with bringing on a CxP early in a project. Finding ways to educate owners about the immediate and long-term value of commissioning is an effort undertaken every day by commissioning professionals.

Who pays the bill?

Best practices recommend that CxPs be hired as a third-party quality assurance provider and owner advocate. Survey results indicate that nearly two-thirds of owners contract commissioning services directly, as shown in Table 2. Although most respondents listed two or more contracting arrangements within their portfolio, 13% indicated they are paid exclusively by owners.

Since A/E design and design-build firms most often hold the primary contract, especially on large projects, it’s not surprising that they come in second as the hiring party, though they rank significantly behind owners.

One company that specializes in BECx said that 55% of its business is subcontracted through a primary mechanical, electrical, and plumbing (MEP) engineering firm.

Generally, lump-sum and fixed-fee contract arrangements are included as part of a turnkey project. Not-to-exceed or time-and-materials contracts predominated for EBCx projects.

Leaders in commissioning

To be accurate, all responsible, engaged CxPs are giants. The firms listed below represent a mere fraction of the providers across the United States who contribute skills, knowledge, and capabilities to make buildings work.

One thing that sets these firms apart is their advocacy, both in terms of their corporate and individual participation and in educational and industry-support activities on behalf of their profession, well beyond their everyday work. Listed in alphabetical order, they are:

- Colliers International

- CxGBS (Commissioning & Green Building Solutions Inc.)

- Dewberry

- Enovity

- Grumman/Butkus

- Horizon Engineering

- McKinstry

- Page/Commissioning

- Primary Integration

- SmartWatt.

One thing is obvious from this survey: Commissioning is conducted by many different entities, focused on a variety of buildings and systems, and not easy to pin down as a professional practice. At the same time, it has become increasingly important as a mechanism for delivering top building performance and is mandated by government entities and private-sector owners alike. The commissioning profession may be diverse, but as a group these firms and individuals are helping to make buildings work better, saving time, financial investment, and resources. That’s gigantic.

Diana Bjørnskov is senior program manager at the Building Commissioning Association. She has spent more than 30 yr in the building industry with extensive experience leading research and analysis of building industry issues, energy policy and legislation, market-potential assessment, and program planning.

Methodology

In June 2015, the Building Commissioning Association (BCA) undertook a survey of CxPs who are "giants" in their field. The nearly 500 firms contacted all make significant contributions to advancing the building industry and high-performance buildings in the built environment.

Here’s what we really wanted to know: who are the CxPs, at what point do CxPs really enter into projects, who hires them and why, how much does it cost, and what’s changing in the markets they serve.

The survey was sent to prequalified corporations across North America, selected from BCA membership, that include commissioning as a major aspect of their professional practice. Seventy-one firms answered the survey. These responding firms represent a cross-section of commissioning business types, all areas of the U.S., and several highly populated areas of Canada.

The majority of respondents (62%) were third-party commissioning firms providing engineering and commissioning or commissioning-only services. They further break out in the survey like this:

- Engineering and commissioning: 35%

- Commissioning-only: 27%

- A/E with internal commissioning group: 13%

- AEC or design-build with internal commissioning group: 12%

- Other (construction management, TAB, project management, peer review, facility inspection and assessment, energy efficiency, program management): 14%