Although cooling from record highs, M&A activity by the 2024 MEP Giants remained robust

Merger and acquisition (M&A) insights

- While deal-making slid from record highs, the 2024 MEP Giants still made mergers and acquisitions a critical component of strategic expansion last year.

- Publicly traded firms were the most active as private equity-backed buyers tapped the brakes.

Booming backlogs, flush balance sheets and robust valuations have sparked a post-pandemic acquisition spree by Consulting-Specifying Engineer’s MEP Giants that continued into 2023. As a group, the largest mechanical, electrical, plumbing (MEP) and fire protection engineering firms completed 54 transactions in 2023 with one-quarter (25%) of the 2024 MEP Giants finalizing at least one deal.

Although merger and acquisition (M&A) activity remained at historically high levels last year, the pace of deal-making by the MEP Giants cooled from the record-setting 70 transactions in 2021 and a still-high 65 deals in 2022. While widespread predictions of a recession and the higher costs of debt that resulted from sharp interest rate hikes as the year progressed likely contributed to the dip in deals in 2023, pricing could also have been a factor.

According to Morrissey Goodale’s propriety database of architecture, engineering (AE) and environmental industry deals, MEP firms in 2023 garnered very strong prices relative to historical norms, which could have deterred MEP Giants pursuing sellers in competitive processes, particularly those that are employee-owned firms.

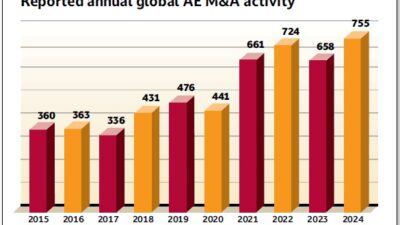

M&A activity by MEP Giants mirrors overall industry

The slight dip in M&A activity among the 2024 MEP Giants reflected the AE and environmental industry. With 658 industry deals worldwide, 2023 was another historically high year for global transactions. While down 9% from the record-high 724 deals in 2022 and slightly behind the 2021 total of 661 transactions, last year’s global M&A deal volume remained a step function above pre-pandemic levels. Domestically, the 444 transactions concluded in 2023 matched the 2021 total and only trailed the 484 deals recorded in 2022, the high-water mark for industry consolidation.

As with the broader AE and environmental industry, Sun Belt firms continue to be the most attractive M&A targets for MEP Giants. With six deals each, California and Florida were the top states where MEP Giants completed acquisitions in 2023. That was followed by New York with five transactions and Texas and Pennsylvania with three each. MEP Giants also concluded nine international deals, led by the purchases of three firms in Australia and two in Canada.

Publicly traded MEP Giants most active buyers

Publicly traded firms were the most prevalent buyers among the 2024 MEP Giants, far outpacing their role in the wider AE and environmental industry. Although publicly traded buyers accounted for just 8% of U.S. domestic AE and environmental industry deals in 2023, these buyers executed 43% of the transactions made by the MEP Giants.

Somewhat surprisingly given recent trends, private equity-backed buyers were responsible for 20% of deals consummated by the MEP Giants in 2023, down slightly from 26% in 2022 but far lower than the 39% of acquisitions attributed to them across the entire industry last year. While employee-owned buyers closed more than half (53%) of AE and environmental industry transactions in 2023, they represented 30% of deals completed by the MEP Giants last year, up from 25% in 2022.

There are several reasons that publicly traded firms have executed the most transactions involving MEP Giants. First, publicly traded firms generally have even easier access to capital than private equity firms, particularly in a higher interest rate environment such as occurred in 2023. The increased cost of debt restricted the available flow of capital from private equity-backed buyers to sellers.

Second, public buyers typically self-finance transactions without the need to borrow money or solicit third-party lenders or other stakeholders beyond the board of directors. Third, data collected by Morrissey Goodale indicate that publicly traded firms, all else being equal, pay more than even private equity-backed firms to complete deals, thus making more attractive offers to sellers.

Bowman most active buyer among MEP Giants

Since its initial public offering in 2021, MEP Giant Bowman (Reston, Virginia) has pursued acquisitions as a key part of its growth strategy, and last year proved no exception. The publicly traded firm, which earlier this year won Morrissey Goodale’s Most Prolific and Proficient Acquirer Award, completed a dozen deals in 2023 that added more than 400 employees in 11 states. That’s on top of the eight transactions it concluded in 2022.

Additional MEP Giants that continued recent buying sprees included IMEG (Rock Island, Illinois), Salas O’Brien (Santa Ana, California) and NV5 (Hollywood, Florida), each of which consummated six transactions. Other MEP Giants that made multiple deals in 2023 were Page (Washington, D.C.), Stantec (Edmonton, Canada), Jensen Hughes (Baltimore), WSP (Montreal, Quebec) and RTM Engineering Consultants (Schaumburg, Illinois).

With 2024 on track to be another stellar year of revenue growth and profitability, unprecedented demand from clients, sustained interest from public equity and substantial public-sector and institutional funding will continue to drive M&A activity among MEP firms. Even the greatest challenge confronting the AE and environmental industry — the talent crunch — carries with it a silver lining for deal-making. As MEP firms struggle to staff all the projects coming through their doors, they are responding not just by investing more in people and technology — but also in acquisitions to quickly boost headcounts.

Since the start of 2021, the domestic AE and environmental industry has experienced a dramatic acceleration in deal-making — with more than a merger a day. Despite geopolitical conflicts abroad and political uncertainty at home, Morrissey Goodale expects the volume of M&A activity to remain elevated in 2024 and beyond as firms look to expand their capabilities, tap into new markets, and gain a competitive edge in an ever-changing business landscape.