The 2016 MEP Giants gross revenue increased compared to last year, most likely due to company mergers and larger and more varied projects. MEP/FP design revenue decreased.

The 2016 MEP Giants generated approximately $47.4 billion in gross annual revenue during the previous fiscal year, a $5.5 billion increase from 2015 in which the firms generated $41.9 billion in gross revenue. This year, the MEP Giants earned $6.11 billion in mechanical, electrical, plumbing, and fire protection (MEP/FP) engineering design revenue, a 10.9% decrease over 2015 revenue.

More than a dozen firms either joined the list for the first time or returned after an absence in reporting data: IPS-Integrated Project Services LLC (No. 11), Middough Inc. (No. 30), Dewberry (No. 32), EwingCole (No. 39), Leach Wallace Associates Inc. (No. 54), Farnsworth Group Inc. (No. 71), Ballinger (No. 75), Westlake Reed Leskosky (No. 86), LaBella Associates D.P.C. (No. 89), The RMH Group (No. 90), Professional Engineering Consultants PA (No. 92), Thorson • Baker + Associates Inc. (No. 95), and Kohler Ronan LLC (No. 98).

A couple of larger firms opted not to participate in the 2016 MEP Giants, particularly Black & Veatch (No. 2 in 2015), and Loring Consulting Engineers Inc. (No. 51 in 2015), which lowered both the gross annual revenue and MEP design revenue for this year. Several mergers and acquisitions occurred in the past year (21%, which was the same as 2015), changing the name and face of many companies and moving some firms up the list due to a larger combined revenue (see page xx for the article "2015 sets new record for industry M&A").

Table 1 shows the top firms based on MEP design revenue, which is how the MEP Giants are ranked. Table 2 shows the top MEP Giants firms based on total gross revenue. The complete table of rankings is provided at www.csemag.com/giants.

About 58.7% of all 2016 MEP Giants’ revenue is generated from MEP design, with an average MEP design revenue of $61.1 million per firm, a drop from $68.6 million in 2015.

Participants indicated that "the economy’s impact on the construction market" is the greatest challenge, though it continues to decrease year over year. For this reporting period, 26% indicated it was a challenge. Last year, 35% said the economy was the biggest corporate challenge; in 2014, 63% of firms reported it as the biggest challenge. Other challenges include "staffing: quality of young engineers" (19%) and "evolving information technologies for design or project management" (14%).

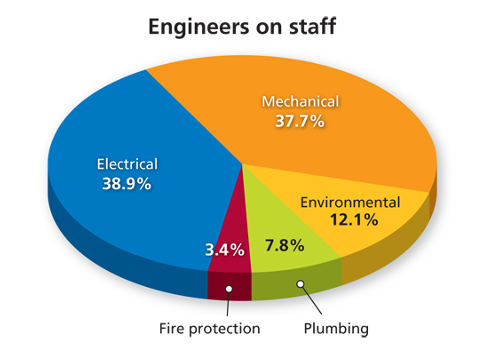

MEP engineering employment numbers

The 2016 MEP Giants firms employ 63,688 engineers, up very slightly from 2015 (63,245 total engineers employed). On average, each 2016 MEP Giants firm has 83 mechanical engineers, 85 electrical engineers, 17 plumbing engineers, 8 fire protection engineers, and 27 environmental engineers on staff. In total, the 2016 MEP Giants have 21,900 engineers on staff (see Figure 1).

In 2016, the MEP Giants earned 83.9% of their MEP design revenue for U.S.-based projects, a slight uptick from 2015. Several opportunities are open to MEP Giants outside the United States. Engineering services are provided in North America (Mexico, Canada) 54% of the time. Other areas of growth include Asia (42% of firms are providing services), the Middle East (33%), the Caribbean (27%), and the European Union (27%). Asian projects have increased over last year and surpassed the Middle East for international work.

When it comes to sustainable engineering, the number of U.S. Green Building Council LEED projects decreased slightly for this reporting period; 1,332 projects were submitted for LEED certification in 2016, where 1,463 projects were submitted in 2015. The number of projects submitted in the past fiscal year to the U.S. Environmental Protection Agency’s Energy Star Buildings Label increased to 347 from 301 projects in 2015.

Project types

The 100 firms listed here don’t handle all aspects of engineering. Many subcontract specialty services including acoustics (63%), security system design (26%), computational fluid dynamics modeling (23%), and construction management (20%). More firms are bringing some specialty services in-house, including controls/building automation systems and/or control sequences and energy modeling.

As shown in Figure 2, MEP Giants indicated that they split their time between new construction (44%) and retrofit/renovation (39%), which has deviated only slightly from past years. Rounding out the projects are maintenance, repair, and operations (7%); commissioning or retro-commissioning (7%); and other (3%). For a more in-depth report on commissioning, read the October 2016 issue on the Commissioning Giants.

The 2016 MEP Giants firms continue to work on several projects in hospitals and health care facilities, office buildings, and schools. Figure 3 breaks down the various building types MEP Giants work in; the health care and office building markets were at the top for this reporting period. Read about several project profiles in a special interactive display at www.csemag.com/giants.

Rounding out the data

Several new questions were introduced in the past couple of years to help provide a better picture of how the MEP Giants firms are managing their businesses. Some interesting facts about the 2016 MEP Giants:

- 62% are privately owned firms; 24% are employee-owned firms.

- The state of New York is home to the most headquarters (13%), with Pennsylvania and Ohio tying for second place with 10% each.

- 2,241 people (on average) account for nonengineering staff at each firm.

- 12.8% of MEP Giants’ engineers are female.

- Aside from standard labor and overhead costs, firms spent the most on new tools (such as software or hardware) in the past fiscal year.

- Top sources of work/contracts come from private owners (via a direct consulting contract), architects and design-build contracts (equal percentage), and government/military.

Methodology

At the beginning of the year, the Consulting-Specifying Engineer (CSE) staff collected and analyzed data from several consulting and engineering firms. Some of the top mechanical, electrical, plumbing, and fire protection (MEP/FP) engineering firms submitted their firms’ profiles to CSE; however, not all consulting firms were willing or able to participate in this year’s MEP Giants survey. The minimum MEP design revenue required for consideration is $5 million, although the smallest firms on this list far exceed that minimum (the smallest firm’s MEP design revenue was $9.3 million).

In 2016, more than 100 engineering firms provided their information for the MEP Giants program, with some newcomers or firms re-entering the program. A tie in the top third (at No. 34) is unusual. Data and percentages are based on the top 100 companies that responded to the request for information; the results do not fully represent the construction and engineering market as a whole. However, with nearly identical questions asked in previous years and more than 100 engineering firms participating this year, we present a qualified portrait of where the top engineering firms stand in 2016.