Building on the prior year’s torrid pace of consolidations, mechanical, electrical, plumbing and fire protection engineering firms announce even more transactions in 2019

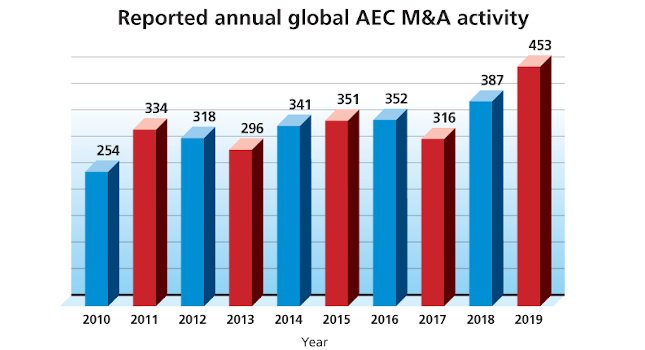

After setting records with 387 deals globally in the architecture, engineering and construction industry in 2018, leaders of industry firms took consolidation to new heights in 2019, notching 453 deals across the globe. The new high-water mark of industry transactions represented a 17% increase over the previous year. The majority of these transactions — or 313 deals — occurred within the United States, making the country the center of industry merger and acquisition activity, a reality driven by the nation’s tremendous economic heft and expectations for robust and sustained demand for engineering services of all types.

Consistent with the industry’s mergers and acquisitions activity, Consulting-Specifying Engineer’s 2019 MEP Giants stepped up their own deal-making last year. The number of deals made by the largest mechanical, electrical, plumbing and fire protection engineering firms rose substantially in 2019 as the group recorded 52 transactions, up 6% from the 49 deals made the year before and up 40% over deal activity in 2017. The multiyear trend indicates sustained interest by the MEP Giants in finding and acquiring firms to achieve long-term business goals.

Acquisitions by MEP Giants in 2019 were led by the usual suspects of repeat acquirers that have made doing deals a core strategy in building and diversifying their firms. Those firms include serial deal-makers NV5 (Hollywood, Fla.) and Salas O’Brien (Santa Ana, Calif.), which, in addition to being mainstays of the MEP Giants list, also regularly rank among the most active acquirers of engineering firms across all sectors in a given year.

But the past year also saw traditionally less acquisitive MEP Giants, such as Integrated Project Services (Blue Bell, Pa.), Bala Consulting Engineers (King of Prussia, Pa.) and PBS Engineers (Glendora, Calif.), enter the deal-making fray. This would indicate growing popularity in acquisitions by a greater range of MEP Giants.

Further, just like the year before, a greater percentage of the MEP Giants in 2019 joined the deal-making party. More than one-quarter of the MEP Giants, 28%, reported a transaction in 2019, up slightly from 2018. This tally is also up considerably from 2017, when just 16% of the industry-leading group notched a deal. With more MEP Giants closing deals, it’s fair to say the macro-level drivers of consolidation facing buyers — increasing competition, the desire for more options to grow and the need to expand in higher-growth geographies — are all at work for MEP Giants.

Drivers of record-breaking deal activity

Before the outbreak of COVID-19, all expectations called for continuing AEC industry consolidation. While the global pandemic certainly affected deal-making, two specific factors helped drive consolidation by MEP Giants in 2019 and we firmly believe those factors will remain in play as the outbreak subsides.

Nontraditional and technology-driven acquisitions. As engineering firms look for ways to differentiate their service offerings and fight back against the commoditization of engineering design, an increasing number of buyers have sought out acquisitions of companies offering services related to engineering, but that are also rooted in applications of technology.

Forward-thinking firm leaders are looking for ways to add value for clients beyond the traditional design process and that increasingly includes investing in niche technology service providers. The following recent deals across the industry and by the MEP Giants provide examples of this trend.

- Tetra Tech acquired GlobalTech, a consulting firm specializing in information technology, cloud migration, cybersecurity and management.

- NV5 acquired The Sextant Group, an information and communications technology and acoustics specialist.

- Ross & Baruzzini acquired COMgroup, a telecommunications consultant.

- Jacobs acquired a 50% share in Simetrica, a research consultancy specializing in social value measurement and well-being analysis.

- Gannett Fleming acquired TTI Consulting, a traffic technology consulting firm with expertise in tolling.

- HED merged with Integrated Design Group, a data center designer.

Private equity capital is here to stay. The emergence of private equity investments in engineering firms has shifted from a trend to a new reality. Last year, private equity deal-making in the domestic U.S. continued to expand as Morrissey Goodale tracked 75 U.S. private equity-backed deals, up from 63 deals in 2018 and 45 deals in 2017. With low long-term interest rates and monetary policy structured by the Federal Reserve to encourage business investment, we expect a low cost of capital to continue to help drive private equity-backed deals, which often rely on debt financing, to a larger share of industry transactions. Active private equity buyers will spur competition for the most attractive deals that might otherwise have gone to the MEP Giants.

M&A in the time of COVID-19

The end of 2019 and start of 2020 brought the world a “black swan” event no one predicted: a global pandemic that drove a voluntary though widespread shutdown of the U.S. and world economies. While most sectors of the economy suffered swift and severe losses, the U.S. engineering industry rapidly adjusted to the new remote work environment and continued to serve clients and execute on projects.

By all accounts, the domestic engineering industry entered the COVID-19 crisis enjoying high demand for services and robust backlogs across a number of market sectors, setting the stage for a reasonable degree of business continuity. However, the uncertainty caused by the pandemic did slow deal-making, with transactions slowed — but not necessarily stopped —by the unprecedented economic disruption.

As of this writing, Morrissey Goodale’s data indicates the crisis sparked by COVID-19 reduced industry transactions on a month-to-month basis by approximately 50% when comparing 2019’s results to deal announcements in year-to-date 2020. We have also observed a shift in approaches to deals in the market. Whereas the MEP Giants closed deals in 2019 with an offensive strategy in mind — one driven by expansion into new markets, territories or technologies (see the list above for examples of the latter) — we expect more deals in the near term to be defensive in nature. This means acquisitions closer to the buyer’s “home turf” or in proven market positions to capture local talent and market share. We also expect acquirers to focus on deals in the states with stronger growth economies and those geographies less affected by COVID-19.

In any case, when the crisis subsides, the drivers of consolidation at work in the industry, including the challenges of increased competition, the need to transition retiring owners and the influence of private equity-backed firms, will still be at work.

For that reason, Morrissey Goodale believes the slump in the number of mergers and acquisitions deals caused by COVID-19 to be temporary and that deal volume will resume as the world adapts to the new, post-COVID reality. Looking ahead, we expect mergers and acquisitions by MEP Giants, while not reaching the record levels of 2019, to return in 2021 to the consistently high levels of the recent past.