The number of transactions in the mechanical, electrical, plumbing and fire protection engineering firms fell sharply in 2020 as compared to prior years, but long-term trends favor escalating M&A activity

Mechanical, electrical and plumbing firms are a class unto themselves in the engineering world, with Consulting-Specifying Engineer’s MEP Giants being the rarest of them all. It’s unusual for one type of engineering firm to run counter to the trends broadly at work in the industry at large.

But if there was ever a year for something unexpected, 2020 was certainly the time and that is exactly what happened with MEP firms in terms of mergers and acquisitions. Last year, with the world in the grips of a global pandemic, engineering firms and the industry as a whole not only survived, but in many cases thrived. This was good news for the engineering business in general and also good news for industry M&A, which continued at a robust pace.

Such performance in 2020 would lead us to believe that the MEP Giants, consistent with the trends in the larger engineering industry, would continue their year long pattern of increasing the number of firms making acquisitions as well as the number of acquisitions made. But as it turned out, the MEP Giants bucked overall industry trends in three critical ways. Specifically:

Trend No. 1: sustained consolidation activity despite the pandemic

In the overall engineering world, buyers and sellers still pursued, closed and announced transactions at a strong pace in 2020. After record-setting levels of merger and acquisition activity in recent years, the architecture and engineering industry closed 425 deals globally in 2020, which was somewhat less than the 453 transactions in 2019, but still more than the 387 deals in 2018.

The majority of the transactions last year occurred within the domestic U.S. — an eye-popping 309 deals — which illustrates the strong economic position of the nation as well as the confidence of industry executives willing to invest in other firms across the country. But while the engineering industry showed a strong appetite for deals in the midst of the uncertainty created by the pandemic, the MEP Giants responded by reducing merger and acquisition activity in 2020.

In fact, the number of the largest mechanical, electrical, plumbing and fire protection engineering firms that reported a deal in the previous year fell to 21%, just over one-fifth of the MEP Giants group. That stands in contrast to 2019, during which 28% of the Giants reported a transaction and 2018, during which 25% of the group closed a deal.

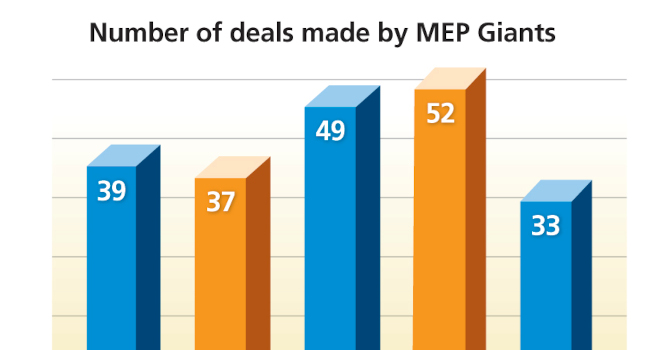

While notable, this data doesn’t tell the full story. As a group in 2020, the MEP Giants recorded 33 transactions, down 37% from the 52 deals made the year before. This also represents a decline from the 49 deals reported in 2018 and the 37 deals reported in 2017. We note, however that while the latest results show a departure from the multiyear trend of increasing acquisitions by the MEP Giants, 2020s activity is still on par with the number of deals made annually by the group just a few years ago.

Trend No. 2: private equity firms are driving deal-making

In the broader engineering industry, the trend before and during 2020 tended to an increasing number of deals being done by private-equity and private-equity-backed firms. Apart from the MEP Giants, this very much held true in the past year, with private equity accounting for more than a quarter of all deals consummated in the U.S. in 2020 and more than one-third of all deals in the U.S. as of this writing in mid-2021.

With private equity having become the preferred equity model for many firms, it is no surprise that owners of firms large and small, having successfully navigated the pandemic year and with near-term prospects for the business still strong, would look to capitalize on their current position to transition or fully exit ownership. An environment in which sellers look to do deals quickly favors skilled, well-capitalized acquirers.

Private equity firms and family offices fit the bill because they are prepared to move swiftly when strategic investments fitting their criteria become available. By contrast, some privately held, employee-owned firms (many of which may be managed by committee) can be slower to make decisions and, though they may be very good acquirers and integrators, simply may not be in a position to strike when the right opportunity presents itself.

Further, larger strategic engineering firms and their management teams may face capitalization challenges of their own stemming from stalled internal ownership transition plans, making investment capital from these buyers even more valuable and their leaders more risk-averse. We anticipate this situation will likely continue to create a favorable landscape for private equity to further grow in the engineering industry in the short and medium term.

However, this is another area in which the MEP Giants bucked the trend as only one private-equity-backed firm, Salas O’Brien (Santa Ana, California), registered a transaction. The other buyers of 2020 consist predominantly of the usual suspects of publicly traded firms Stantec (Edmonton, Alberta) and WSP (Montreal, Quebec) and stalwart employee stock ownership plan or employee-owned firms IMEG (Rock Island, Illinois) and LaBella Associates (Rochester, New York).

Nonetheless, given the high level of interest in the engineering sector from private equity firms, we expect to see more financial buyers involved in MEP deals going forward.

Trend No. 3: the number of buyers in the engineering space is increasing

Recent years have brought us a diverse group of buyers from all sectors and geographic corners of the market, inclusive of private equity buyers, publicly traded strategic buyers, ESOPs and midsize and smaller employee-owned engineering firms. We would expect the same for MEP firms but based on the data, it was only a few big, brave MEP Giants that shrugged off the pandemic and kept on acquiring.

If we use tallies of transactions as a measure of confidence, a handful of serial acquirers expressed supreme optimism throughout 2020. Specifically, industry leaders IMEG and Salas O’Brien recorded eight and five transactions, respectively, during the course of the year. These buyers by themselves represented nearly 40% of the 33 transactions closed by the MEP Giants in 2020.

Well-known MEP industry names Stantec, WSP and Jacobs (Dallas) also notched multiple transactions, whereas NV5 (Hollywood, Florida) and Gannett Fleming (Camp Hill, Pennsylvania), both of which were quite active in 2019, scaled back deal-making in the pandemic year.

So what does this mean for the future of M&A activity of the MEP Giants? The critical point is that the long-term drivers of consolidation, which were present long before the pandemic, are still very much in play and, if anything, have intensified over the last year. For buyers, those factors include the need to address mounting competitive pressures, the goal to expand in high-growth geographies and the desire to capture increasing government spending on infrastructure.

Sellers, meanwhile, will continue to face challenges with their internal ownership and leadership transition while seeking to capitalize on strong valuations in the current marketplace. Therefore, in 2021 and beyond, acquisitions will remain a critical part of the growth strategies — and business opportunities — for the MEP Giants.

Reported annual global AEC M&A activity

Percent of MEP Giants reporting a deal

Number of deals made by MEP Giants