Industry consolidation continues to shape the competitive environment for MEP engineering firms. The biggest MEP Giants are getting bigger. Is this good for our industry?

Almost 20% of the Consulting-Specifying Engineer 2011 MEP Giants merged with, sold to, or acquired another architecture, engineering, or construction (AEC) firm or non-AEC entity over the past year. When you stop to think about it, this is a stunning statistic in and of itself—one-fifth of the leading mechanical, electrical, plumbing (MEP), or fire protection engineering firms pursued growth through consolidation with another firm. However, the storylines behind this statistic are where the implications for the industry’s MEP firms are to be found.

Consolidation is here to stay

This year’s rate of consolidation among the MEP Giants continues the torrid pace seen over recent years and provides further confirmation that this is a long-term corrective force here to stay. Two years ago, we noted that one in five of the major players in the MEP industry participated in a merger or acquisition, while last year this statistic jumped to more than one quarter of the MEP Giants. The results from this year confirm that consolidation among the MEP Giants, their peers, and competitors is here to stay.

What’s driving this consistent level of consolidation among MEP firms? Well, for any deal to happen there must be a willing buyer and a willing seller who see a strategic or business fit in the marriage and who can agree on a price. The recent and continuing challenging market environment for the domestic design and construction industry has created a greater pool of willing sellers. These firms are typically smaller engineering firms that have seen their earnings reduced, holes punched in their balance sheets, and backlogs shrunk by the soft economy. After hanging on for two years for the “recovery” to take effect, management and owners in these firms realized their chances of riding out the “new normal” were growing slimmer and slimmer. For these firms, a sale or merger became the most attractive and—in some cases—the only viable alternative to a shutdown of operations.

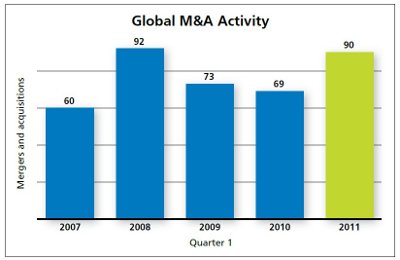

Based on all the deal-making activity that has been reported so far in 2011, you can expect to see many more management teams make the same choice. Through the first quarter of 2011, 90 merger and acquisition deals were announced in the global AEC industry, representing a 30% increase over levels seen through the first quarter of 2010 (see Figure 1). From 2007 to 2010, 28% of total deals were announced in the first quarter. Should this same trend continue in 2011, the industry is on pace for 321 total deals to be consummated in 2011 (see Figure 2), surpassing the record-breaking levels of 2008 (303 deals). We can expect a similar increase in deals in the MEP space. Domestically, the increase in deal pace is somewhat slower with merger and acquisition activity up 12% over the first six months of last year. This is a reflection of the relatively slow pace of the U.S. economic recovery as compared with the faster-expanding economies in Asia and South America.

Mergers and acquisitions as a growth strategy

One interesting facet of this resurgence in industry consolidation in 2010 and 2011 is the use of mergers and acquisitions by skilled and motivated acquirers as a growth strategy. As the industry started to move into and navigate through the recession, the percentage of domestic deals occurring across state lines (where the buyer and seller are headquartered in different states) plummeted to 54% to 60%—down from its traditional level of between 66% and 75%.

In 2011 it looks like that trend is going to be reversed. In the first quarter of this year, almost two-thirds (64%) of domestic deals have occurred across state lines (see Figure 3). This represents the highest level of interstate activity since 2006 and provides a hint that the industry is returning to growth-focused mergers and acquisitions as opposed to the defensive deal-making of recent times. The acquisition by integrated architecture, engineering, and planning firm and MEP Giant HGA Architects and Engineers (Minneapolis) of architecture, interior design, and planning firm Wisnewski Blair & Assoc,. Ltd. (Alexandria, Va.) is a great example of this trend, as was the acquisition of California architecture firm WWCOT (Santa Monica, Calif.) by MEP Giant DLR Group (Omaha, Neb.).

The big get bigger

Perhaps the most interesting aspect of the deal-making activity on the part of the MEP Giants is that of the 19 firms involved in a merger or acquisition, 18 of them were the acquirers in the deals that were done. This means that the largest providers of professional MEP engineering services in the country continued to consolidate their leading position through the addition of smaller firms.

Seven out of the top 10 MEP Giants—representing 56% of the dollar value of MEP revenues generated by the top 100—made acquisitions in the past year. While many MEP firms struggled to find growth in the soft economy, these industry giants used their strong balance sheets to acquire their way into new market sectors, expand their geographic footprint, and deepen their bench of talented technical professionals.

A key part of this consolidation of MEP services revenues (and therefore earnings and profits) among the biggest firms in the industry is the influence and activity of publicly traded design firms. Five of the 2011 MEP Giants are either publicly traded firms or subsidiaries of a publicly traded firm. All five of these firms made acquisitions in the past year, including URS’s acquisition of the United Kingdom’s Scott Wilson Group and AECOM’s acquisitions of the United Kingdom’s David Langdon and Springfield, Va.-based McNeil Technologies. It’s a given that these publicly traded firms will continue to make acquisitions as this is the primary way for them to support the growth required to drive the value of their stock.

Morrissey is managing principal of Morrissey Goodale LLC, a management consulting and research firm based in Newton, Mass., with offices in Phoenix and Denver, that serves the AEC industry exclusively. An engineer by training, Morrissey has assisted numerous MEP firms in the areas of strategy development and implementation, leadership development and transition, technical and professional talent recruitment, ownership transition, and mergers and acquisitions.

Are mergers and acquisitions good or bad for the industry?

I’m often asked whether this trend of consolidation is a good thing or a bad thing for our industry. We all hear so many negative stories about mergers: how folks who had built their careers at a firm left soon after it was sold because they didn’t like the new work environment for whatever reason (e.g., too impersonal, too different, or too financially focused, or the new parent firm killed the family-friendly culture that they were used to). Or they left because the new owners didn’t see the value in them and fired them or laid them off. I take all of these anecdotes with a grain of salt and relate them to the old saying about client service—that you are eight times more likely to hear about poor client service than good client service. Similarly, I believe that you are more likely to hear negative stories about acquisitions than positive ones. The negative stories just tend to get more “airtime.”

So, instead of dwelling on the negative, I like to answer the question as to whether industry consolidation is changing the industry for better or worse by examining it from three different perspectives.

Project owners: The first is the project owners’ perspective. As a project owner, I want reliability and competency from my MEP engineer, and I want to feel confident that they will be there to meet my needs through the project lifecycle and beyond if necessary. I would argue that larger, well-capitalized firms are in a better position to meet these needs. Larger firms should be able to provide owners with a broader range of services and deeper level of expertise. They should also be more stable over the long haul as their capital structure should in theory remove the ownership transition and associated capitalization challenges faced by smaller firms. Similarly, with a greater ability to invest in training and development, larger firms should be better able to build a talented, skilled, cutting-edge team than smaller firms. So, from an owner’s perspective, I believe over time, industry consolidation is a good thing.

The MEP professional: The second perspective is that of the MEP professional. Many (most?) professionals that work for smaller, employee-owned, privately held firms indicate—when asked what they like about their firm—that they like the people that they work with, the firm’s culture, and the autonomy that they have. All of these are powerful and positive characteristics of smaller, privately held firms. On the flip side, all things being equal, larger firms tend to be able to provide their employees with higher salaries and better benefits. Also, in this rapidly globalizing industry, larger firms are in a better position to provide their professionals with the opportunity to work on exciting and challenging international projects, which have a better chance of actually getting to construction than many domestic projects. So, it’s unclear to me if this wave of consolidation will be a good thing for the engineering professional. In large part it will be a subjective decision based on his or her motivations and values.

Industry influence: Finally, I like to view consolidation in the context of the strength of the overall AEC industry—particularly as it relates to its influence on the economy and society. I believe that current industry associations do a terrific job of representing the industry’s interests. However, I believe our industry could have even greater influence on public policy making if there were an increased amount of larger, publicly traded AEC firms in the ranks of the Fortune 500 and 1000. With a greater number of AEC firms on the publicly traded exchanges, our industry will have greater visibility and clout with lawmakers and society in general. So, ultimately, from an industry perspective, I believe consolidation is a good thing.